Understand the 50/30/20 budgeting rule for Indians in 2025—spend 50% on needs, 30% on wants, and save 20% for future goals to balance life and finances.

In bustling cities like Bengaluru, with rents and living costs climbing ever higher, budgeting isn’t just smart—it’s necessary. A viral story on Reddit highlighted a 22-year-old engineer managing to live comfortably on ₹20,000/month in Bengaluru, using sensible allocation and clever hacks like room sharing, public transport, and DIY meals.

His expense breakdown? ₹8,000 on food, ₹9,000 on rent, ₹2,000 on travel, and ₹2,000 for essentials. While he chose a no-frills lifestyle, his monthly discipline and sacrifices resonated with Indians across income brackets facing city inflation and stagnant wages.

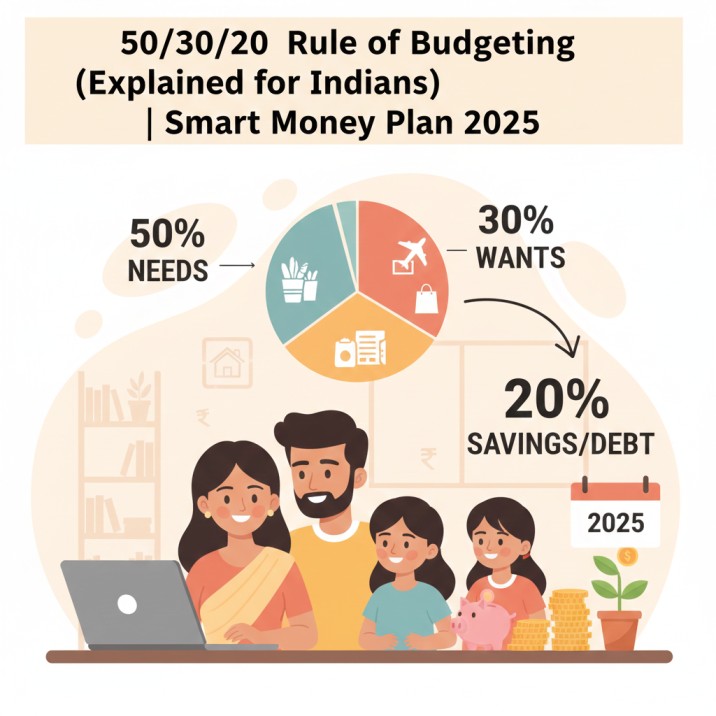

50/30/20 Rule of Budgeting (Explained for Indians) | Smart Money Plan 2025

Managing money can feel confusing for many Indians. Salaries arrive every month, but expenses such as rent, groceries, EMIs, fuel, and entertainment quickly consume most of it. By the end of the month, many people wonder where their money went.

This is where a simple budgeting method like the 50/30/20 rule can make a big difference.

The 50/30/20 rule is one of the most popular budgeting frameworks used worldwide. It divides your monthly income into three clear categories: needs, wants, and savings. Instead of complicated spreadsheets, it gives you an easy structure to manage your money.

For Indian families dealing with rising living costs, this rule helps create a balanced approach to spending and saving.

In this beginner-friendly guide, we will explain how the 50/30/20 rule works for Indian incomes, how to apply it in real life, and how it can help you build a stronger financial future.

💡 Personal Experience

A few years ago, I realised that despite earning regularly, I was saving very little. When I started following a simple budgeting structure similar to the 50/30/20 rule, I could finally see where my money was going—and my monthly savings improved within a few months.

You can also explore more practical strategies in our guide on saving money tips at

https://savewithrupee.com/15-daily-money-hacks-to-save-₹10000-this-year/

What Is the 50/30/20 Budget Rule?

The 50/30/20 rule is a simple budgeting formula that divides your monthly income into three categories.

| Category | Percentage | Purpose |

|---|---|---|

| Needs | 50% | Essential expenses |

| Wants | 30% | Lifestyle spending |

| Savings | 20% | Savings and investments |

This system was popularised by US Senator Elizabeth Warren in her book All Your Worth: The Ultimate Lifetime Money Plan.

Even though it originated in the US, the rule works very well for Indian households with small adjustments.

Understanding the Three Categories

1. Needs (50%)

Needs are expenses that are necessary for survival and daily living.

Examples include:

- Rent or home loan EMI

- Groceries

- Electricity and water bills

- Mobile and internet bills

- Transportation

- School fees

- Insurance premiums

If you stop paying these expenses, your basic lifestyle will be affected.

Example

If your monthly salary is ₹40,000, your essential expenses should ideally stay within ₹20,000.

2. Wants (30%)

Wants are expenses that improve your lifestyle but are not strictly necessary.

Examples include:

- Eating out

- Online shopping

- Movies and OTT subscriptions

- Travel and vacations

- Gadgets and fashion purchases

These expenses bring comfort and enjoyment but can be controlled when necessary.

For example, ordering food from delivery apps frequently can increase this category. You can reduce such spending with smart strategies. Learn more in our guide on

https://savewithrupee.com/how-to-save-on-food-delivery-apps-zomato-swiggy/ savewithrupee.sitemap.march 09

3. Savings and Investments (20%)

This category focuses on your future financial security.

Examples include:

- Emergency fund savings

- Mutual fund SIPs

- Fixed deposits

- Retirement investments

- Stock market investments

- Gold savings

Financial experts recommend saving at least 20% of income, though saving more is always better.

If you want to start small investments, explore our guide on best investment options in India at

https://savewithrupee.com/mutual-fund-vs-fixed-deposit-which-is-better-in-india-2025-complete-beginners-guide/

How the 50/30/20 Rule Works for Different Indian Salaries

Let’s see practical examples.

| Monthly Income | Needs (50%) | Wants (30%) | Savings (20%) |

|---|---|---|---|

| ₹20,000 | ₹10,000 | ₹6,000 | ₹4,000 |

| ₹30,000 | ₹15,000 | ₹9,000 | ₹6,000 |

| ₹50,000 | ₹25,000 | ₹15,000 | ₹10,000 |

| ₹80,000 | ₹40,000 | ₹24,000 | ₹16,000 |

For many Indians living in big cities, essential expenses may exceed 50%. In such cases, small adjustments can still help maintain the spirit of the rule.

Step-by-Step Guide to Implement the 50/30/20 Rule

Step 1: Calculate Your Monthly Income

Start by calculating your net monthly income (after tax).

Example:

Salary after deductions = ₹45,000

Step 2: List All Expenses

Write down every monthly expense such as:

- Rent

- Groceries

- Fuel

- Phone bills

- Subscriptions

Tracking expenses helps you understand spending patterns.

A simple system can help you track spending effectively. Learn more in our monthly budgeting guide at

https://savewithrupee.com/how-i-manage-my-own-monthly-budget-in-india-my-real-2025-example-with-actual-numbers/

Step 3: Categorise Expenses

Divide your expenses into three groups:

Needs

- Rent

- Groceries

- Utilities

Wants

- Restaurants

- Entertainment

- Online shopping

Savings

- SIP investments

- Emergency fund

- Retirement savings

Step 4: Adjust Spending

If your spending looks like this:

| Category | Current Spending |

|---|---|

| Needs | 65% |

| Wants | 25% |

| Savings | 10% |

Then you should try to:

- Reduce unnecessary wants

- Increase savings gradually

Step 5: Automate Savings

Automation makes saving easier.

For example:

- Set automatic SIP investments

- Transfer money to savings on salary day

You can also explore strategies in our guide on passive income ideas at

https://savewithrupee.com/passive-income-ideas-in-india-2025-12-real-ways-to-earn-while-you-sleep/

Comparison Table: 50/30/20 Rule vs Traditional Budgeting

| Feature | 50/30/20 Rule | Traditional Budget |

|---|---|---|

| Complexity | Simple | Often complicated |

| Categories | 3 main groups | Many small categories |

| Flexibility | High | Moderate |

| Beginner friendly | Yes | Sometimes difficult |

| Tracking required | Minimal | Detailed |

The biggest advantage of the 50/30/20 rule is simplicity.

Real-Life Example: Middle-Class Indian Family

Consider a family earning ₹60,000 per month.

| Category | Budget | Example Expenses |

|---|---|---|

| Needs | ₹30,000 | Rent, groceries, utilities |

| Wants | ₹18,000 | Dining out, entertainment |

| Savings | ₹12,000 | SIP, emergency fund |

By following this structure, the family gradually builds financial stability.

An important part of financial stability is having emergency savings. Learn how to build one in our emergency fund guide at

https://savewithrupee.com/emergency-fund-how-much-should-an-indian-household-keep-practical-guide-2025/

Common Mistakes Indians Make with Budgeting

1. Ignoring Small Expenses

Small daily expenses like tea, snacks, and subscriptions add up.

2. Not Tracking Spending

Without tracking expenses, budgeting becomes ineffective.

3. Saving What’s Left Over

Many people save money after spending, which rarely works.

A better approach is saving first.

4. Lifestyle Inflation

As income increases, spending often increases as well.

This reduces long-term savings.

Expert Tips for Using the 50/30/20 Rule in India

Start with a Flexible Version

If 50% for needs is unrealistic, try:

60 / 20 / 20

Reduce Fixed Expenses

Examples:

- Move to cheaper housing

- Reduce subscriptions

- Cook at home more often

Increase Income

Additional income sources can make budgeting easier.

You can explore ideas in our guide on

passive income ideas at

https://savewithrupee.com/passive-income-ideas-in-india-2025-12-real-ways-to-earn-while-you-sleep/

Pros and Cons of the 50/30/20 Rule

| Pros | Cons |

|---|---|

| Easy to understand | May not fit very low incomes |

| Flexible structure | Needs discipline |

| Encourages savings | Urban expenses may exceed 50% |

| Good for beginners | Not very detailed |

Frequently Asked Questions

1. Does the 50/30/20 rule work for low incomes in India?

Yes, but adjustments may be needed. Some people use 60/20/20 or 70/20/10 depending on expenses.

2. Should EMI payments be included in needs?

Yes. Home loan, personal loan, and car EMIs are essential expenses.

3. What if my expenses exceed 50%?

This is common in big cities. Try reducing lifestyle spending or increasing income gradually.

4. Can students use the 50/30/20 rule?

Yes. Students can apply it to manage pocket money or stipends.

5. Is saving 20% enough?

Saving 20% is a good starting point, but higher savings will accelerate financial growth.

6. How do I start investing with my savings?

You can begin with options like mutual fund SIPs, which allow investments starting from ₹500 per month.

Conclusion

The 50/30/20 rule is one of the easiest ways to manage money without complicated budgeting systems.

By dividing your income into:

- 50% for essential needs

- 30% for lifestyle wants

- 20% for savings and investments

you create a balanced financial plan that supports both present comfort and future security.

For Indians trying to improve their financial habits in 2025, this rule offers a practical starting point.

You don’t need a perfect budget from day one. Even small changes—like reducing unnecessary spending and increasing savings—can create long-term financial stability.

The goal is simple: spend wisely today so you can live more comfortably tomorrow.

References

- Reserve Bank of India – Household Financial Savings Reports

https://www.rbi.org.in - SEBI – Investor Education Resources

https://www.sebi.gov.in - Investopedia – 50/30/20 Budget Rule

https://www.investopedia.com - Economic Times – Personal Finance and Budgeting Trends in India

https://economictimes.indiatimes.com

Author Insight

In my own experience managing monthly expenses in India, I realized that the biggest financial problems were not due to low income, but due to lack of planning. For example, when my monthly income was around ₹25,000, I often ended up spending almost everything without saving anything at the end of the month.”

“I started tracking my expenses daily using a simple notebook. Within one month, I noticed that small, unnecessary expenses like frequent online orders and unplanned spending were taking a large portion of my income.”

“By making small changes—like setting a fixed budget for groceries, limiting online purchases, and saving at least ₹2,000 at the beginning of each month—I was able to reduce financial stress and slowly build better control over my money.” “These are simple and practical methods that any Indian household can follow without needing complex financial knowledge.”

Research Sources

- Reserve Bank of India – Financial Reports

- SEBI Investor Education

- Economic Times – Personal Finance

- Investopedia – Budgeting & Finance Basics

Disclaimer: This article is based on personal experience and is for educational purposes only. It does not constitute financial, investment, or legal advice. Readers are advised to do their own research or consult a qualified professional before making any financial decisions.