A powerful money lesson taught by Indian parents — explained simply. Learn how one life-changing financial advice shaped long-term habits, savings, investment discipline, and how it can change your future too.

💡 Strong Intro

Indian parents may not know complex finance, but their wisdom comes from experience, struggle, sacrifice, and real-life money battles.

Sometimes, a single line from them becomes a lifelong financial anchor.

For me, there was one money advice my parents told me that completely changed my life.

I didn’t realise its power when I first heard it.

But today, every saving, investment, and financial decision I make goes back to that one sentence.

This is not just my story — it’s the story of millions of Indians who grow up in middle-class homes filled with love, responsibility, and practical wisdom.

Let’s dive into the advice, why it’s so powerful, how it can transform your life, and the steps to apply it immediately.

⭐ Key Takeaways

- Indian parents often give timeless financial wisdom

- The best money advice is usually simple, practical, and habit-based

- Small financial discipline builds long-term wealth

- Saving consistently matters more than income level

- Real wealth comes from avoiding mistakes, not chasing returns

- This advice can be applied by students, salaried, homemakers & families

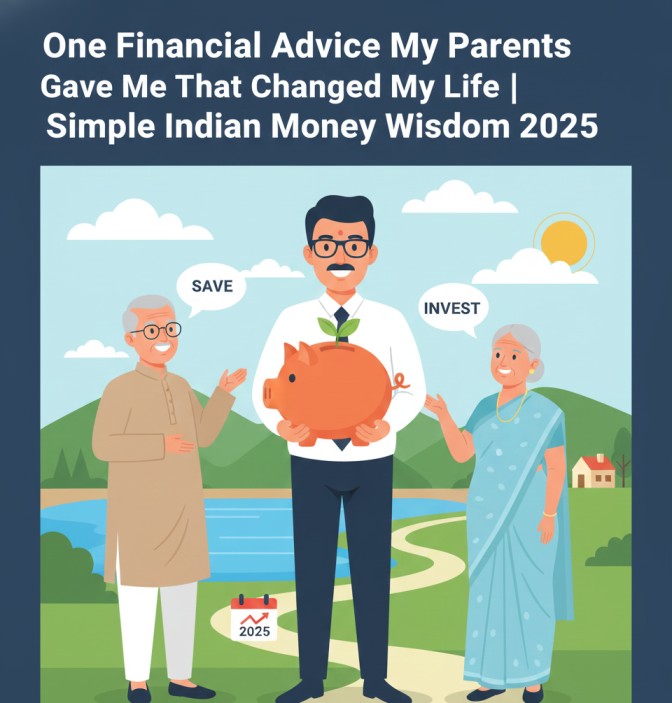

❤️ The One Financial Advice My Parents Gave Me

My parents told me:

“Beta, always save first, spend later. If you start late, even God can’t help your finances.”

It sounded harsh.

But it became the single most important financial principle of my life.

For years, I used to:

- Spend first

- Save “whatever was left”

- Delay investing

- Avoid planning

- Live month-to-month

This advice flipped my life.

Because saving first forces you to build discipline — a value that builds real wealth.

If you struggle with savings, this will help:

👉 50-30-20 Rule for Indians

https://savewithrupee.com/50-30-20-rule-of-budgeting-explained-for-indians/

💭 Why This Simple Advice Changes Everything

✔ Because it gives you control over your money

When you save first, expenses have to adjust — not your goals.

✔ Because it builds emergency power

Life stops feeling scary.

👉 Emergency Fund Guide:

https://savewithrupee.com/emergency-fund-how-much-should-an-indian-household-keep-practical-guide-2025/

✔ Because it removes money stress

You stop feeling guilty every month.

✔ Because it builds habits, not just savings

Small amounts → Big habits → Big wealth.

✔ Because the earlier you start, the bigger the compounding

Time is the biggest multiplier.

🧘 The Indian Middle-Class Mindset Behind the Wisdom

Indian parents grow up seeing:

- Job loss

- Medical emergencies

- Struggle to pay school fees

- Loans ruining peace

- Unexpected family responsibilities

- Rising costs

- Pressure to support relatives

They understand one truth:

“Stability is bigger than income. Savings are bigger than salary.”

This advice comes from experience, not textbooks.

🇮🇳 Real Indian Stories (5 People, Same Lesson)

Here are 5 stories from normal Indians who realised the power of the same advice.

Story 1: Ritu (Student) – “₹20 a day changed my life”

Ritu started saving ₹20 daily because her mother told her:

“Always keep something for yourself.”

Today, she has her first emergency fund of ₹15,000.

It helped her during a sudden travel need.

Also read:

👉 Student Budget Hacks

https://savewithrupee.com/student-budget-hacks-save-pocket-money-smartly/

Story 2: Prakash (Delivery Partner) – “One breakdown taught him everything”

He didn’t save anything.

His bike broke down → borrowed money → paid high interest.

Later, his father told him the same advice:

“Save before spending.”

He now keeps an emergency fund + RD.

👉 FD vs RD guide

https://savewithrupee.com/fd-vs-rd-which-is-better-for-indians/

Story 3: Shalini (Teacher) – “SIP became her habit”

Her parents taught her to always save first.

She started a ₹500 SIP during her first job.

Today, she has over ₹3 lakh saved slowly and steadily.

👉 SIP for Beginners

https://savewithrupee.com/sip-for-beginners-start-with-₹500/

Story 4: Arjun (IT Employee) – “Job loss woke him up”

He earned well but saved nothing.

One layoff changed him.

He followed his mother’s advice: save first.

Today, he has a 6-month emergency fund + investments.

Story 5: Priya (Homemaker) – “The kitchen taught her finance”

She saved ₹10–₹30 from groceries every day.

Over years, it turned into real wealth and confidence.

👉 Grocery savings

https://savewithrupee.com/grocery-shopping-tips-to-cut-monthly-expenses/

🪜 How You Can Apply This Advice in 2025

Here is the exact step-by-step plan you can copy:

Step 1: Calculate your basic expenses

Rent, groceries, EMIs, school fees, transport.

Step 2: Save 10–20% immediately when salary comes

Move it to a separate account.

Step 3: Build a 3–6 month emergency buffer

Use RD if needed for discipline.

Step 4: Start one SIP

Even ₹500 is enough.

Step 5: Increase savings every 6 months

₹200–₹300 extra makes a huge difference.

Step 6: Automate everything

No thinking → no forgetting → no skipping.

💰 Saving vs Investing — What Parents Really Mean

Indian parents aren’t anti-investment.

They are anti-risk.

Here is what they actually want:

| Parents Say | Actual Meaning |

|---|---|

| “Save first” | Build emergency fund & discipline |

| “Don’t waste money” | Avoid lifestyle pressure |

| “Think before buying” | Prioritize needs over wants |

| “Save for future” | Invest long-term |

Most of them would fully support SIPs, PPF, gold savings, and safe investments.

👉 Wealth Building (Slow & Simple)

https://savewithrupee.com/how-to-build-wealth-slowly-in-india/

📊 Comparison Tables

1. Saving When You Get Salary vs Saving Whatever Is Left

| Method | Result |

|---|---|

| Save first | Wealth, stability, confidence |

| Save later | Stress, regret, no growth |

2. Instruments That Help You “Save First”

| Instrument | Risk | Good For |

|---|---|---|

| FD | Low | Short-term goals |

| RD | Low | Monthly discipline |

| SIP | Medium | Long-term wealth |

| Gold Savings | Medium | Inflation-proof saving |

| PPF | Very Low | 15-year forced saving |

3. Where to Keep Savings vs Where to Invest

| Purpose | Best Option |

|---|---|

| Emergency | Savings + FD |

| 1–3 years | RD / Low-risk funds |

| 5+ years | SIP / PPF |

| Very low income | RD / Small savings schemes |

👉 Low-cost saving options:

https://savewithrupee.com/best-low-cost-saving-schemes-in-india-2025-for-beginners-start-small-save-smart/

👍 Pros & Cons of Following This Advice

Pros

- Stress-free money life

- Strong financial foundation

- No dependence on loans

- Peace during emergencies

- Easy long-term wealth creation

- Works for all income levels

Cons

- Requires discipline

- Takes time to see results

- You may feel restricted initially

- Needs patience

⚠️ Common Mistakes I Made Before Understanding the Advice

- Saving only when salary increased

- Not tracking expenses

- Zero emergency fund

- Buying unnecessary things

- Confusing wants with needs

- Listening to random financial tips

- Avoiding SIP due to fear

- Taking costlier EMIs to “look successful”

Avoid these traps →

👉 5 Money Mistakes Indians Make in Their 20s

https://savewithrupee.com/5-money-mistakes-indians-make-in-their-20s/

🛠️ Tools & Apps That Helped Me Follow This

- SBI YONO (FD/RD automation)

- Zerodha / Groww (SIP automation)

- Google Sheets (budgeting)

- Money Manager (tracking expenses)

- UPI Lite for small payments

👉 https://savewithrupee.com/upi-lite-explained-save-while-you-pay-small/

🔗 Read Our Other Articles

- Wealth Building

https://savewithrupee.com/how-to-build-wealth-slowly-in-india/ - Emergency Funds

https://savewithrupee.com/emergency-fund-how-much-should-an-indian-household-keep-practical-guide-2025/ - Savings on Small Salary

https://savewithrupee.com/how-to-save-money-on-a-small-salary-₹10000-₹20000-full-practical-indian-guide-2025/ - Budgeting & Money Discipline

https://savewithrupee.com/best-free-budgeting-apps-in-india-2025-edition/ - SIP Basics

https://savewithrupee.com/sip-for-beginners-start-with-₹500/

🎯 Who This Is For

- Students beginning financial habits

- Young professionals

- Newly married couples

- Low-income families

- Homemakers

- Anyone who wants long-term peace & stability

📋 Quick Checklist

✔ Save first, spend later

✔ Build emergency fund

✔ Start SIP

✔ Keep separate accounts

✔ Avoid lifestyle pressure

✔ Increase savings yearly

✔ Track expenses

✔ Follow long-term discipline

❓ FAQs

1. What is the best financial advice for beginners?

Save first, spend later — the foundation of wealth.

2. Is saving more important than investing?

Yes, in the beginning. Investing comes after savings discipline.

3. How much should I save monthly?

10–20% is ideal; start small and build slowly.

4. Why do Indian parents focus on savings so much?

They’ve seen financial instability first-hand; they value safety.

5. Can this advice work even for low-income people?

Yes — even ₹10–₹20/day builds strong habits.

🧾 Final Summary

Indian parents may not talk about mutual funds, stock markets, or financial apps, but their simple advice often contains the deepest wisdom.

“Save first, spend later.”

This one line can change your future, your habits, your peace, and your entire financial life — just like it changed mine.

Start small.

Start simple.

Start today.

Your future self will silently thank your parents for this timeless advice.

Disclaimer: This article is based on personal experience and is for educational purposes only. It does not constitute financial, investment, or legal advice. Readers are advised to do their own research or consult a qualified professional before making any financial decisions.