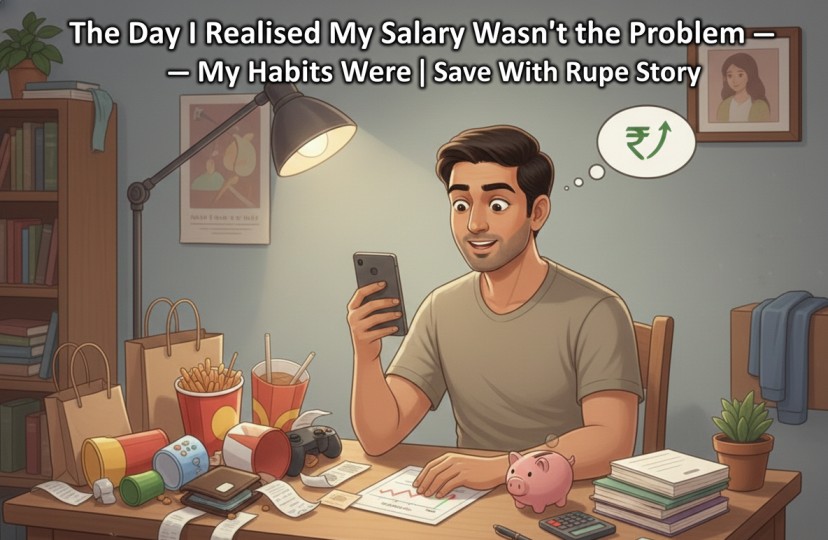

I blamed my low salary for years. One honest realisation changed my financial life forever. A real Indian money story by Save With Rupee’s founder.

💔 The Day I Realised My Salary Wasn’t the Problem — My Habits Were

(A real Indian money awakening story)

For years, I believed one thing very strongly:

“If only my salary was higher, my life would be sorted.”

I complained when my salary was ₹18,000.

I complained again when it became ₹30,000.

Even at ₹45,000, peace never came.

If you’re reading this and nodding silently — this article is for you.

This is not a motivational speech.

This is not a “work harder” lecture.

This is the most honest money realisation of my life — the day I stopped blaming my salary and finally looked at my habits.

🙋♂️ About Me (So You Know This Is Real)

My name is H. Suresh,

a finance content creator from Chennai, Tamil Nadu.

For over 10 years, I’ve researched:

- Indian saving techniques

- Practical budgeting

- Side income ideas

- Digital opportunities that actually work

I started SaveWithRupee.com with one simple belief:

Smarter Money. Better Life. One Rupee at a Time.

No jargon.

No hype.

No unrealistic promises.

Just real Indian money lessons — often learned the hard way.

😔 My Old Belief: “Salary Kam Hai, Isliye Problem Hai”

Like most middle-class Indians, I grew up hearing:

- “Job stable honi chahiye”

- “Salary badhegi toh sab theek ho jayega”

- “Paise kam hain, isliye stress hai”

So naturally, I believed income was the root of all problems.

But something strange kept happening…

🔁 Salary Increased, Stress Stayed

Phase 1: ₹18,000 Salary

- End of month = zero balance

- Borrowing before payday

- No savings

I thought: “Normal hai, salary hi kam hai.”

Phase 2: ₹30,000 Salary

- Better phone

- More eating outside

- Random online shopping

Still:

- No emergency fund

- Still waiting for next salary

I thought: “Abhi family responsibilities hain.”

Phase 3: ₹45,000 Salary

This is where reality slapped me.

I had:

- A decent income (for that time)

- No major EMIs

- No dependents

Yet I was still anxious.

That’s when I asked myself a dangerous question:

“If salary is the problem, why does stress grow with income?”

⚡ The Day of Realisation (My Turning Point)

One evening in Chennai, during a power cut (very symbolic),

I checked my bank statement carefully.

Not emotionally.

Not defensively.

Honestly.

And what I saw shocked me.

🧾 What My Bank Statement Revealed

- Food delivery apps — regularly

- Impulse shopping — frequent

- Subscriptions I barely used

- No planned savings

- No emergency fund

- No investing

The truth hit me hard:

My salary wasn’t leaking.

My habits were bleeding it.

😶 The Most Painful Truth I Accepted

I wasn’t “bad with money” because:

- I earned less

But because: - I spent without thinking

- I saved only leftovers

- I avoided tracking

- I used spending as stress relief

That day, I stopped lying to myself.

📉 Real-Life Habit #1 That Hurt Me: No Expense Tracking

I used to say:

“Mujhe yaad rehta hai main kahan kharch karta hoon.”

Reality?

I remembered big expenses, not daily leaks.

₹150 here.

₹300 there.

₹99 subscriptions.

👉 This changed everything for me:

How My Life Changed After Tracking My Expenses

📱 Habit #2: Emotional Spending (Silent Killer)

Bad day at work?

→ Order food.

Stress?

→ Buy something online.

Lonely?

→ Shopping “reward”.

I wasn’t buying things.

I was buying temporary relief.

😔 Habit #3: Saving After Spending (Big Mistake)

I used to think:

“End of month jo bachega, save karunga.”

Guess what remained?

Nothing.

This single habit delayed my financial stability by years.

🧠 The Mental Shift That Changed Everything

One simple thought rewired my brain:

“If I don’t control habits at ₹30,000,

I won’t control them at ₹1,00,000.”

That day, I stopped chasing salary hikes blindly

and started fixing my system.

🪜 The Step-by-Step Changes I Made (Very Simple)

✅ Step 1: I Tracked Every Rupee (30 Days)

No judgement.

Only awareness.

👉 Tools helped, but pen-paper worked too.

Best Free Budgeting Apps in India

✅ Step 2: I Built a Tiny Emergency Fund

Not 6 months.

Just ₹10,000 first.

That small buffer reduced anxiety massively.

👉 Guide that helped me later:

Emergency Fund – How Much Do You Need?

✅ Step 3: I Automated Savings (Even Small)

I started SIP with ₹500.

Not impressive.

But powerful.

👉 Beginner-friendly:

SIP for Beginners – Start with ₹500

✅ Step 4: I Reduced Lifestyle Noise

Not lifestyle.

Lifestyle noise.

- Fewer impulse buys

- Conscious spending

- Clear priorities

🧍♂️ Realisation #2: Habits Are Louder Than Income

I saw people earning:

- Less than me → saving more

- More than me → stressed & broke

The difference?

Habits. Not salary.

This connects deeply with:

Why Most Indians Never Feel Rich No Matter How Much They Earn

🔄 Myth vs Reality (From My Own Life)

| Myth ❌ | Reality ✅ |

|---|---|

| Salary will fix everything | Habits decide outcome |

| Saving is painful | Overspending is painful |

| I’ll start later | Later never comes |

| Tracking is boring | Stress is worse |

⚠️ Mistakes I Personally Made (Learn From Me)

- ❌ Ignored small expenses

- ❌ No emergency fund

- ❌ Emotional shopping

- ❌ No clear money goal

- ❌ Compared lifestyle with others

👉 Related lesson:

My Biggest Regret About Money

✅ Do vs Avoid Table (Based on My Experience)

| Do ✅ | Avoid ❌ |

|---|---|

| Track expenses | Guessing |

| Save first | Saving leftovers |

| Spend consciously | Emotional spending |

| Start small | Waiting for perfect time |

🧾 Simple Checklist That Changed My Life

✔ Expense tracking started

✔ Emergency fund building

✔ One SIP active

✔ Reduced impulse spending

✔ Clear monthly plan

If you tick 3, you’re ahead of where I was.

👍 Pros & Cons of Fixing Habits First

Pros

- Works at any income

- Immediate stress reduction

- Builds discipline

- Sustainable long-term

Cons

- Requires honesty

- Initial discomfort

- No instant gratification

🏆 Editor’s Pick (My Core Belief Today)

“Money problems are rarely about money.

They’re about behaviour.”

This belief is the foundation of SaveWithRupee.com.

❓ FAQs (Based on Messages I Receive)

1. Can habits really beat low salary?

Yes. Habits decide how far salary goes.

2. When should I start saving?

The day you earn your first rupee.

3. Is tracking really necessary?

Yes. Awareness precedes control.

4. How small can I start?

Even ₹100 saved consciously matters.

5. Did you become rich after this?

No. I became peaceful first.

6. What if family pressure exists?

Systems help manage emotions & expectations.

7. What’s the first habit to fix?

Expense tracking.

❤️ Final Words (From Me to You)

If you feel:

- Stuck despite earning

- Guilty about spending

- Anxious about future

Please know this:

You are not bad with money.

You were just never taught.

I created SaveWithRupee.com so you don’t have to learn everything the hard way like I did.

🚀 Strong Call To Action (CTA)

If my story felt familiar, don’t stop here.

👉 Start with this simple, life-changing guide:

7 Steps to Become Financially Independent

Bookmark SaveWithRupee.com

— where Indian money advice is honest, practical, and human.

Smarter Money. Better Life. One Rupee at a Time. 💚

Author Insight

In my own experience managing monthly expenses in India, I realized that the biggest financial problems were not due to low income, but due to lack of planning. For example, when my monthly income was around ₹25,000, I often ended up spending almost everything without saving anything at the end of the month.”

“I started tracking my expenses daily using a simple notebook. Within one month, I noticed that small, unnecessary expenses like frequent online orders and unplanned spending were taking a large portion of my income.”

“By making small changes—like setting a fixed budget for groceries, limiting online purchases, and saving at least ₹2,000 at the beginning of each month—I was able to reduce financial stress and slowly build better control over my money.” “These are simple and practical methods that any Indian household can follow without needing complex financial knowledge.”

Research Sources

- Reserve Bank of India – Financial Reports

- SEBI Investor Education

- Economic Times – Personal Finance

- Investopedia – Budgeting & Finance Basics

Disclaimer: This article is based on personal experience and is for educational purposes only. It does not constitute financial, investment, or legal advice. Readers are advised to do their own research or consult a qualified professional before making any financial decisions.