Understand the 50-30-20 rule for Indian families in 2025. Learn how to divide income smartly between needs, wants, and savings — with real examples, tools, and tips.

📋 Table of Contents

- 🧮 What Is the 50-30-20 Rule?

- Why This Budgeting Rule Fits the Indian Middle Class

- 💡 How to Calculate Your 50-30-20 Budget Step-by-Step

- 📊 Example: Family with ₹60,000 Monthly Income

- 🧠 Benefits of Following the 50-30-20 Rule in 2025

- 🧾 Common Mistakes Indians Make While Budgeting

- 💼 How to Customize This Rule for Your Lifestyle

- 🔗 Internal SaveWithRupee Guides to Build a Smarter Budget

- ⭐ Editor’s Pick – SaveWithRupee Team Recommends

- ❓ Frequently Asked Questions (FAQs)

- 🧭 Final Word – Budget Smart, Live Free

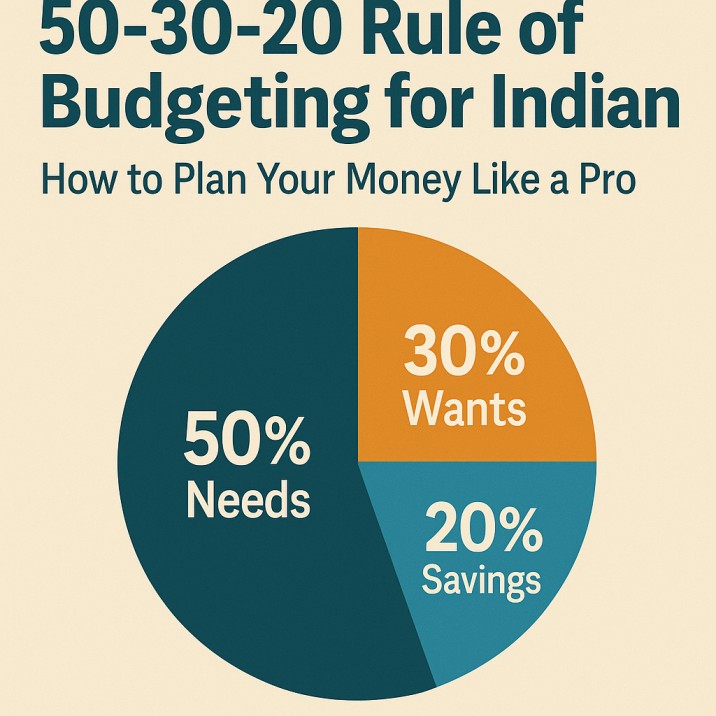

🧮 1. What Is the 50-30-20 Rule?

The 50-30-20 rule is one of the simplest and most effective budgeting frameworks in the world.

It divides your net income (after tax) into three parts:

| Category | Purpose | Recommended % |

|---|---|---|

| 🏠 Needs | Rent, food, EMIs, bills | 50% |

| 🎉 Wants | Dining out, entertainment, shopping | 30% |

| 💰 Savings & Investments | SIPs, FDs, insurance, emergency fund | 20% |

💬 In short: Spend smart, enjoy life, and invest for the future.

It’s not about restricting yourself — it’s about controlling money before it controls you.

🇮🇳 2. Why This Budgeting Rule Fits the Indian Middle Class

India’s middle class is the backbone of the economy — hardworking, aspirational, and always juggling multiple responsibilities.

The 50-30-20 rule fits perfectly because:

✅ It balances lifestyle and savings — no extreme frugality.

✅ It helps plan for irregular incomes (bonus, festival expenses).

✅ It’s adaptable to small-town or metro living.

For example, a family following this rule can easily create an Emergency Fund and still enjoy occasional luxuries like weekend outings.

💡 3. How to Calculate Your 50-30-20 Budget Step-by-Step

Let’s break it down:

Step 1: Identify Monthly Net Income

Include all earnings — salary, freelancing, or side hustles.

💼 Read: Best Side Hustles in India 2025 to add extra cash flow.

Step 2: Allocate 50% for Needs

This includes essentials:

- House rent/loan

- Groceries

- Utilities (electricity, water, mobile recharge)

- Transport/fuel

- School fees

💡 Control costs using How to Reduce Your Electricity Bill in India 2025.

Step 3: Allocate 30% for Wants

Enjoy guilt-free spending — movies, travel, or eating out.

Just cap it at 30%.

Use rewards and cashback to stretch this section:

👉 How to Earn ₹500 Daily with Cashback Apps.

Step 4: Allocate 20% for Savings & Investments

Start SIPs, build your emergency fund, or invest in low-cost schemes.

Use tools from Best Free Budgeting Apps in India 2025 Edition to track.

📊 4. Example: Family with ₹60,000 Monthly Income

| Category | % | Amount (₹) | Example Expenses |

|---|---|---|---|

| Needs | 50% | ₹30,000 | Rent (12k), groceries (8k), bills (5k), transport (5k) |

| Wants | 30% | ₹18,000 | Dining out, OTT, kids’ hobbies, weekend trips |

| Savings/Investments | 20% | ₹12,000 | SIP (₹5000), RD (₹2000), insurance (₹3000), emergency fund (₹2000) |

💬 Even on ₹60k income, this family can save ₹1.44 lakh/year while living comfortably.

If your income is lower, use 60-20-20 (more for needs).

If higher, shift to 40-30-30 to build wealth faster.

🧠 5. Benefits of Following the 50-30-20 Rule in 2025

✅ Simple & Visual: Easy to understand, no complex formulas.

✅ Builds Discipline: Automates savings without thinking.

✅ Balances Lifestyle: You can spend freely without guilt.

✅ Financial Awareness: Makes you conscious of where every rupee goes.

✅ Helps Beat Inflation: Prioritizing investing ensures your money grows faster than expenses.

💡 Combine this method with Smart Investment Habits of Middle-Class Indians for maximum growth.

🧾 6. Common Mistakes Indians Make While Budgeting

- Mixing Needs & Wants:

Buying a new phone “because you need it” — but do you really? - No Emergency Fund:

One medical bill can destroy a year’s savings. Build yours first. - Ignoring Small Recurring Charges:

Netflix, OTT, and app subscriptions quietly eat ₹1000+/month.

See: Hidden Bank Charges You’re Paying Every Month. - Not Tracking Spends:

You can’t fix what you don’t measure.

Use free tools from Best Budgeting Apps in India. - Neglecting Insurance:

Don’t forget — savings vanish fast without protection.

Check: How to Save on Insurance Premiums.

💼 7. How to Customize This Rule for Your Lifestyle

The 50-30-20 rule is flexible — here’s how to tweak it:

| Life Stage | Custom Ratio | Example Focus |

|---|---|---|

| Students | 60-20-20 | Lower income, fewer bills |

| Newly Married Couples | 45-25-30 | Focus on investments |

| Families with Kids | 55-25-20 | Education + EMIs |

| Retirees | 40-30-30 | Healthcare & stability |

| Freelancers/Self-employed | 40-40-20 | Variable income; save more |

Adapt, don’t abandon. The key is consistency.

💬 Budgeting is personal — the math stays, the meaning changes.

🔗 8. Internal SaveWithRupee Guides to Build a Smarter Budget

- Monthly Budget Plan for Family with ₹30,000 Income

- Why Family Budget Plan Is Important

- 15 Daily Money Hacks to Save ₹10,000 This Year

- 10 Lifestyle Changes That Will Save You Money in 2025

- Best Low-Cost Saving Schemes in India 2025

⭐ 9. Editor’s Pick – SaveWithRupee Team Recommends

🟢 Smart Investment Habits of Middle-Class Indians – Build Wealth Step-by-Step

📈 Learn to grow your savings into real assets.

🟢 Passive Income Ideas in India 2025 – Make Money While You Sleep

💤 Convert your savings into recurring income.

🟢 Hidden Bank Charges You’re Paying Every Month – Stop Losing Money in 2025

⚠️ Keep your hard-earned rupees safe from invisible deductions.

🟢 Best Side Hustles in India 2025 – Earn ₹10,000/Month

💼 Boost your income to strengthen your budget.

🟢 Emergency Fund – How Much Should You Keep?

💰 Protect your family from financial shocks.

❓ 10. Frequently Asked Questions (FAQs)

Q1. How does the 50-30-20 rule work for irregular income?

If your income varies, average your last 3 months and use 50-30-20 as a flexible guide — invest only after covering essentials.

Q2. What if my needs exceed 50% of income?

Shift to 60-20-20 temporarily, then reduce EMI, rent, or bills over time.

Q3. Can I apply this rule with my spouse’s income?

Yes — combine both incomes and categorize total expenses under the same rule.

Q4. How can students use this rule?

Use 60-20-20: 60% for study/living costs, 20% for enjoyment, 20% savings (even ₹500 SIP counts).

Q5. Is this rule suitable for small-town India?

Absolutely. It’s even easier to follow since expenses are lower. You can save more (up to 30%).

Q6. Should I count loan EMIs under needs or savings?

Home/car EMIs count as “needs” since they’re fixed obligations. But investments like SIPs or RDs go under “savings.”

🧭 11. Final Word – Budget Smart, Live Free

A good budget doesn’t feel like punishment — it feels like control.

When you give every rupee a purpose, you never wonder “where did my money go?” again.

💬 Start this month — open a notebook or budgeting app, note your income, and apply the 50-30-20 rule.

Within three months, you’ll notice your savings growing without cutting joy.

The secret isn’t earning more — it’s managing better.

💚 SaveWithRupee Says:

“A budget isn’t about limitation — it’s about freedom.”

Next, read:

👉 Smart Investment Habits of Middle-Class Indians – Build Wealth Step-by-Step in 2025

and

👉 Passive Income Ideas in India 2025 – Make Money While You Sleep