For many salaried Indians, salary credit day feels like a mini celebration. After weeks of managing limited cash, seeing the bank balance increase suddenly brings relief. But what happens next often determines whether the rest of the month will be financially smooth or stressful.

In many households, the first few days after salary credit are when most financial mistakes happen. Bills get paid, shopping begins, subscriptions renew, and sometimes impulse spending starts quietly. By the middle of the month, the bank balance drops faster than expected.

This cycle repeats every month for thousands of salaried professionals across India. The issue is rarely about earning too little. Instead, it’s about how money is handled immediately after salary arrives.

The first 3–5 days after salary credit are the most important for budgeting. If money is managed wisely during this period, the rest of the month becomes easier.

In this article, we will explore the most common budgeting mistakes salaried Indians make right after salary credit day and practical solutions to avoid them.

Personal Experience

“Earlier, the first weekend after salary credit used to be my biggest spending period. Online orders, eating out, and random purchases quietly reduced my balance before I even realised it.”

“Once I started allocating money immediately after salary credit—rent, savings, and essential expenses—the rest of the month became much easier to manage.”

Why Salary Credit Day Is Financially Dangerous

When salary arrives, people often feel financially comfortable again.

Psychologists call this “income illusion” — the temporary feeling that you have plenty of money.

This leads to decisions like:

- Ordering food frequently

- Buying things online

- Upgrading gadgets

- Paying for subscriptions impulsively

Within a few days, spending momentum builds.

Without proper planning, a large portion of the salary disappears in the first week.

Common Budgeting Mistakes After Salary Credit

Let’s examine the most common financial mistakes.

1. Not Allocating Money Immediately

Many people leave their entire salary in one account and start spending from it.

This makes it difficult to know how much money is actually available for spending.

A better approach is immediate allocation.

Example after salary credit:

| Category | Allocation |

|---|---|

| Rent/EMI | Fixed amount |

| Savings | 10–20% |

| Household expenses | Planned budget |

| Personal spending | Limited amount |

This method creates clear spending boundaries.

2. Spending First, Saving Later

One of the biggest mistakes Indians make is saving whatever is left at the end of the month.

But in reality, there is usually nothing left.

The correct approach is:

Salary → Savings → Expenses.

Even saving ₹2000 first can build financial discipline.

If you’re new to saving, you can explore beginner options here:

Learn more in our guide on best investment options in India at

https://savewithrupee.com/sip-for-beginners-start-with-₹500/

3. Weekend Lifestyle Spending

The first weekend after salary credit is when many people overspend.

Common activities include:

- Restaurants

- Shopping malls

- Online purchases

- Entertainment subscriptions

While enjoying your salary is important, uncontrolled spending in the first week damages the entire month’s budget.

A better strategy is to create a fixed monthly lifestyle budget.

4. Ignoring Upcoming Monthly Expenses

Many people forget expenses that occur later in the month.

Examples include:

- Electricity bills

- School fees

- Mobile recharge

- Grocery restocking

- Fuel costs

Without planning for these expenses, money may run out early.

A clear budgeting plan prevents this problem.

You can build one using structured budgeting methods here:

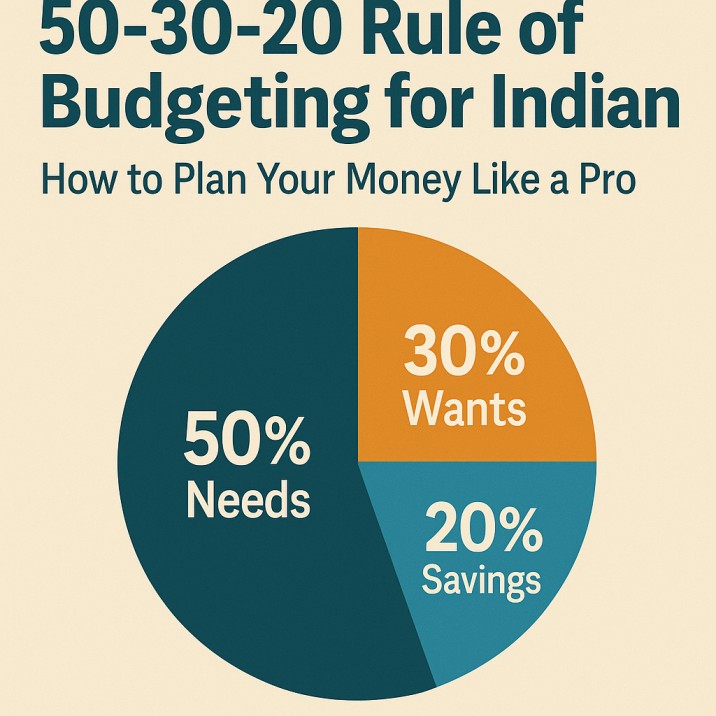

Learn more in our guide on monthly budgeting guide at

https://savewithrupee.com/50-30-20-rule-of-budgeting-for-indians-in-2025-how-to-plan-your-money-like-a-pro/

5. Ignoring Small Spending Leaks

Small daily spending can destroy budgets quickly.

Examples:

- Food delivery

- Coffee and snacks

- Cab rides instead of public transport

- Online impulse purchases

Individually these seem small, but monthly they can add up to ₹3000–₹8000.

You can learn more about these spending leaks here:

Learn more in our guide on saving money tips at

https://savewithrupee.com/where-most-indian-households-lose-money-without-realising-hidden-leaks-explained/

6. Not Keeping an Emergency Buffer

Unexpected expenses can happen anytime:

- Medical issues

- Vehicle repairs

- Travel emergencies

Without a financial buffer, these expenses disrupt your budget.

Experts recommend building an emergency fund that covers 3–6 months of expenses.

Learn how to create one here:

Learn more in our guide on emergency fund guide at

https://savewithrupee.com/emergency-fund-for-indian-families-how-much-you-really-need-where-to-keep-it-savewithrupee/

7. Using Credit Cards Too Easily

Credit cards are convenient but dangerous when spending is not tracked.

Many people use them heavily after salary credit because they feel financially secure.

However, the real bill appears next month.

This creates a cycle where future income is already spent.

Step-by-Step Guide to Handle Salary Credit Day Smartly

Here is a simple system to follow every month.

Step 1: Save Immediately

The first action after salary credit should be savings.

Example:

Salary: ₹40,000

Savings allocation:

₹4000–₹8000 (10–20%)

Transfer it immediately.

Step 2: Pay Fixed Expenses First

Next, handle unavoidable expenses.

Examples:

- Rent

- EMIs

- Insurance

- School fees

Once these are paid, you know the real available balance.

Step 3: Allocate Weekly Spending Limits

Divide remaining money weekly.

Example:

Remaining monthly spending money: ₹12,000

Weekly limit: ₹3000.

This prevents overspending early in the month.

Step 4: Set Aside an Emergency Buffer

Keep a small buffer amount.

Example:

₹2000–₹5000 monthly buffer.

This protects your budget.

Step 5: Plan Lifestyle Spending

Enjoy your money — but with limits.

Example:

- Restaurants

- Shopping

- Entertainment

Create a separate budget for these expenses.

Comparison of Salary Management Methods

| Feature | No Budget System | Basic Budget | Structured Budget |

|---|---|---|---|

| Spending control | Poor | Medium | Strong |

| Savings consistency | Low | Medium | High |

| Financial stress | High | Medium | Low |

| Works for beginners | No | Yes | Yes |

Structured budgeting dramatically improves financial control.

Real-Life Example: A ₹45,000 Salary Professional

Consider Ankit, an IT employee in Pune.

Before Budgeting

| Expense | Amount |

|---|---|

| Rent | ₹12,000 |

| Groceries | ₹7000 |

| Transport | ₹4000 |

| Lifestyle spending | ₹12,000 |

| Savings | ₹0 |

By the 20th of every month, his bank balance was nearly zero.

After Salary-Day Budgeting

| Category | Amount |

|---|---|

| Savings | ₹6000 |

| Fixed expenses | ₹22,000 |

| Variable expenses | ₹12,000 |

| Buffer | ₹5000 |

Within one year he built ₹70,000 savings.

Common Mistakes to Avoid

Avoid these salary-day financial mistakes.

Ignoring Expense Tracking

Without tracking, budgets fail.

Buying Big Items Immediately

Delay large purchases by a few days.

Not Planning for Festivals

Festival expenses often disrupt budgets.

Ignoring Savings

Savings must be automatic.

Expert Tips for Salary-Day Budgeting

Follow the “24-Hour Rule”

Before buying something expensive, wait 24 hours.

Impulse purchases often disappear after waiting.

Use Separate Bank Accounts

One account for salary, one for spending.

This improves control.

Track Expenses Weekly

Weekly reviews prevent budget damage.

Increase Income Slowly

Side income can strengthen finances.

Explore realistic options here:

Learn more in our guide on passive income ideas at

https://savewithrupee.com/passive-income-ideas-in-india-2025-12-real-ways-to-earn-while-you-sleep/

Pros and Cons of Strict Salary-Day Budgeting

| Pros | Cons |

|---|---|

| Better financial control | Requires discipline |

| Reduces monthly stress | Needs planning |

| Improves savings | Takes time to develop habit |

| Prevents overspending | Some lifestyle adjustments needed |

Frequently Asked Questions

1. Why is the first week after salary dangerous financially?

Because people feel temporarily wealthy and overspend.

2. What should be the first thing after salary credit?

Savings allocation.

3. How much should I save monthly?

Experts suggest 20% of income, but even 5–10% is a good start.

4. Should I avoid all spending after salary credit?

No. Just control spending and follow a budget.

5. Is cash budgeting better?

For many people, cash spending reduces impulsive purchases.

6. How can I reduce impulse shopping?

Use waiting rules and fixed monthly budgets.

7. Can budgeting increase savings significantly?

Yes. Even small monthly savings grow over time.

Conclusion

Salary credit day can either strengthen your financial future or quietly damage it.

The difference lies in how the money is managed during the first few days.

By saving first, allocating expenses properly, controlling lifestyle spending, and planning for unexpected costs, you can avoid the common mistakes that many salaried Indians make.

Financial stability is not about earning the highest salary. It is about managing income wisely and building consistent financial habits.

If you handle salary credit day correctly, the rest of the month becomes far easier to manage.

References

Reserve Bank of India Financial Reports

https://www.rbi.org.in

SEBI Investor Education Resources

https://www.sebi.gov.in

Economic Times Personal Finance Section

https://economictimes.indiatimes.com/wealth

Investopedia Budgeting Basics

https://www.investopedia.com/budgeting-4689745

Personal Experience

“Over the years, I’ve noticed that most financial problems don’t come from low income, but from lack of planning and awareness. Even small changes in spending habits can make a big difference.”

“In my own journey, tracking expenses and following a simple budget helped me reduce stress and gain better control over money. These are practical lessons any Indian household can apply.”

Research Sources

- Reserve Bank of India – Financial Reports

- SEBI Investor Education

- Economic Times – Personal Finance

- Investopedia – Budgeting & Finance Basics

Disclaimer: This article is based on personal experience and is for educational purposes only. It does not constitute financial, investment, or legal advice. Readers are advised to do their own research or consult a qualified professional before making any financial decisions.