Introduction

For many Indian households, the biggest financial frustration is simple: the salary finishes before the month ends.

Whether someone earns ₹20,000, ₹50,000, or even ₹1 lakh per month, the same feeling often exists — expenses keep rising faster than income. Rent increases, school fees go up every year, groceries become expensive, and unexpected medical or family costs appear regularly.

This is the financial reality for millions of Indians. According to several household finance surveys and RBI data, a large percentage of Indian families live with very little monthly surplus. Saving money often feels impossible.

But budgeting is not about cutting every small joy in life. A practical Indian budget focuses on control, awareness, and smarter spending, not extreme sacrifice.

In this article, we will look at:

- Why many Indians feel their salary is never enough

- A realistic approach to budgeting in India

- A simple step-by-step system to manage money even with limited income

- Real examples from Indian households

- Common mistakes that keep people stuck financially

If you feel that your income is always falling short, this guide will help you take control of your finances in a practical way.

Understanding the Problem: Why Salary Feels Never Enough

In theory, budgeting sounds simple — earn money, spend less, save the rest.

In real life, especially in India, the situation is very different.

Most families face three major financial pressures.

1. Fixed Expenses Are Increasing

Many essential costs keep rising:

- House rent

- Electricity bills

- School fees

- Transport fuel

- Groceries

Even if salary increases by 5–10% per year, inflation often eats that increase.

2. Hidden Monthly Expenses

Small spending leaks quietly drain money:

- Food delivery

- Online shopping

- Multiple mobile subscriptions

- Impulse purchases

- Festival expenses

Many households lose ₹2000–₹5000 monthly without realizing it.

If you want to understand this problem deeper, read our detailed article on hidden spending leaks:

Learn more in our guide on saving money tips at https://savewithrupee.com/where-most-indian-households-lose-money-without-realising-hidden-leaks-explained/

3. Lack of Structured Budgeting

Most Indians manage money mentally rather than with a clear plan.

Money flows like this:

Salary → Bills → Random expenses → End of month struggle.

Without a structure, saving becomes accidental instead of intentional.

A strong starting point is building a proper system.

Learn more in our guide on personal finance planning at https://savewithrupee.com/the-only-money-system-an-indian-family-needs-simple-sustainable-stress-free/

Key Benefits of Budgeting (Even on a Small Salary)

Budgeting is often misunderstood as restriction. In reality, it creates financial freedom and clarity.

Here are the biggest benefits.

1. You Know Exactly Where Money Goes

Many people feel poor not because income is low but because expenses are unclear.

Tracking spending reveals financial leaks instantly.

2. Financial Stress Reduces

When you know your money plan, anxiety reduces dramatically.

Unexpected expenses become easier to handle.

3. Saving Becomes Automatic

Even saving ₹1000 per month consistently can grow over time.

4. Better Financial Decisions

Budgeting helps you decide:

- When to buy

- When to delay

- What expenses are unnecessary

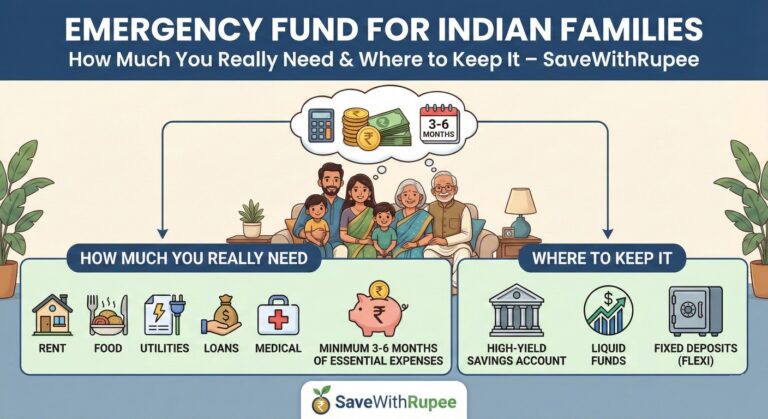

5. Builds Emergency Security

Without budgeting, most families never build emergency savings.

You can learn how to build one in this detailed guide:

Learn more in our guide on emergency fund guide at https://savewithrupee.com/emergency-fund-for-indian-families-how-much-you-really-need-where-to-keep-it-savewithrupee/

Step-by-Step Guide: How to Budget When Salary Is Tight

Budgeting must be simple enough to follow every month.

Here is a practical system that works for most Indian households.

Step 1: Calculate Your Real Monthly Income

Start with your actual take-home salary, not the CTC.

Example:

| Income Source | Amount |

|---|---|

| Salary | ₹35,000 |

| Freelance income | ₹5,000 |

| Total monthly income | ₹40,000 |

Always budget based on minimum guaranteed income.

Step 2: Identify Essential Expenses

Essential expenses are non-negotiable.

Examples:

- Rent or home loan

- Groceries

- Utilities

- School fees

- Transport

Example breakdown for ₹40,000 income:

| Expense | Amount |

|---|---|

| Rent | ₹10,000 |

| Groceries | ₹6,000 |

| Transport | ₹3,000 |

| Utilities | ₹2,000 |

| School fees | ₹3,000 |

Total essentials: ₹24,000

Step 3: Track Spending for 30 Days

Before cutting expenses, observe your spending.

Use:

- A simple notebook

- Google Sheets

- Budget apps

You will quickly notice patterns like:

- Frequent Swiggy orders

- Online impulse purchases

- Unused subscriptions

Many people reduce spending naturally after seeing the numbers.

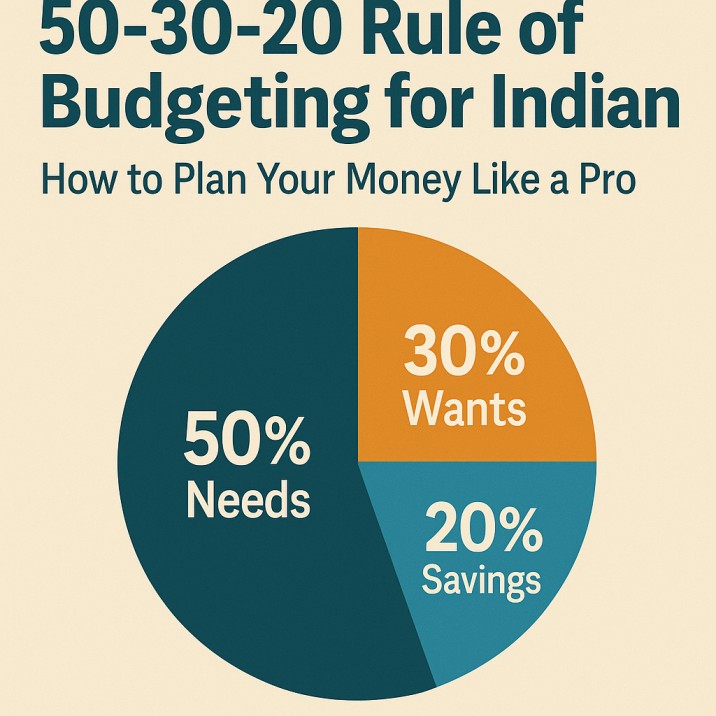

Step 4: Follow a Realistic Budget Rule

The popular budgeting rule worldwide is 50-30-20.

But for most Indian families, this needs modification.

Practical Indian Budget Rule

| Category | Percentage | Example (₹40,000 income) |

|---|---|---|

| Needs | 60% | ₹24,000 |

| Wants | 20% | ₹8,000 |

| Savings | 20% | ₹8,000 |

But if savings feel difficult initially, start with 5–10% savings.

Learn more about this method in our guide on monthly budgeting guide at

https://savewithrupee.com/50-30-20-rule-of-budgeting-for-indians-in-2025-how-to-plan-your-money-like-a-pro/

Step 5: Use the Envelope Method

This is one of the simplest budgeting systems used in many Indian households.

Divide money into categories:

- Grocery envelope

- Transport envelope

- Entertainment envelope

- Household expenses envelope

Once the envelope is empty, no more spending in that category.

You can also read our detailed explanation here:

Learn more in our guide on saving money tips at https://savewithrupee.com/a-simple-envelope-budget-system-that-actually-works-for-indian-homes/

Step 6: Automate Small Savings

Saving should happen immediately after salary arrives.

Examples:

- ₹2000 monthly SIP

- ₹1000 recurring deposit

- ₹500 emergency fund

Even small amounts matter.

If you want to start investing slowly, check this beginner-friendly article:

Learn more in our guide on best investment options in India at https://savewithrupee.com/sip-for-beginners-start-with-₹500/

Comparison: Different Budgeting Methods for Indians

| Feature | Traditional Budget | Envelope System | 50-30-20 Method |

|---|---|---|---|

| Ease of use | Medium | Very Easy | Easy |

| Best for beginners | No | Yes | Yes |

| Control on spending | Medium | High | Medium |

| Requires apps | Sometimes | No | Optional |

| Works with low salary | Limited | Excellent | Good |

For most Indian families, envelope budgeting works best initially.

Real-Life Example: A ₹30,000 Salary Household

Let’s take a realistic case.

Ravi, a private employee in Coimbatore, earns ₹30,000 monthly.

Before Budgeting

Expenses looked like this:

| Expense | Amount |

|---|---|

| Rent | ₹9000 |

| Groceries | ₹6000 |

| Transport | ₹3000 |

| Random spending | ₹8000 |

| Remaining | ₹4000 |

But most months, he ended with zero savings.

After Budgeting

He started using envelope budgeting.

| Category | Amount |

|---|---|

| Essentials | ₹20,000 |

| Personal spending | ₹5,000 |

| Savings | ₹3,000 |

| Emergency fund | ₹2,000 |

Within 12 months, Ravi saved ₹60,000.

Small structure created big change.

Common Budgeting Mistakes Indians Make

Avoid these mistakes if you want budgeting to work.

1. Unrealistic Budgets

If your budget cuts everything, you will abandon it quickly.

Budget must allow small enjoyment expenses.

2. Ignoring Annual Expenses

Examples:

- School admission fees

- Festivals

- Insurance payments

These must be planned monthly.

3. Not Tracking Spending

Without tracking, budgeting becomes guesswork.

4. Using Credit Cards Without Discipline

Credit cards can destroy budgets if spending isn’t tracked.

5. Trying to Save Too Much Initially

Start small.

Consistency matters more than big numbers.

Expert Tips for Managing Money on a Tight Salary

1. Focus on Expense Optimization

Sometimes reducing expenses is easier than increasing income.

Examples:

- Reduce food delivery

- Use public transport

- Cook more meals at home

2. Increase Income Slowly

Small side income can transform finances.

Examples:

- Freelancing

- Tuition classes

- Online micro-tasks

You can explore more ideas here:

Learn more in our guide on passive income ideas at https://savewithrupee.com/passive-income-ideas-in-india-2025-12-real-ways-to-earn-while-you-sleep/

3. Use Weekly Budgets

Weekly budgeting helps prevent mid-month money shortages.

4. Build Financial Awareness

Just reading about money regularly improves financial habits.

Pros and Cons of Strict Budgeting

| Pros | Cons |

|---|---|

| Better control over money | Requires discipline |

| Reduces financial stress | Needs regular tracking |

| Helps build savings | Can feel restrictive initially |

| Improves spending habits | Takes time to master |

The key is flexible budgeting, not rigid rules.

Personal Experience

“A few years ago, I used to wonder why my salary always disappeared before the month ended. Only when I started tracking every rupee did I realise the problem wasn’t just my income — it was my habits.”

“One simple notebook where I wrote down daily expenses changed my entire financial mindset. Small leaks like food delivery and impulse shopping were quietly draining thousands every month.”

“Budgeting didn’t suddenly make me rich. But it gave me control. For the first time, I knew exactly where my money was going and how to improve it.”

Frequently Asked Questions

1. What if my salary is too small to budget?

Budgeting is actually more important for small salaries. Even managing ₹20,000 wisely can create savings.

2. How much should Indians save monthly?

Ideally 20%, but even 5–10% savings is a good start.

3. Is budgeting necessary for single people?

Yes. Singles often overspend because they don’t track expenses.

4. Should couples create a joint budget?

Yes. Financial transparency reduces money conflicts.

5. What is the biggest budgeting mistake?

Not tracking daily expenses.

6. Are budgeting apps necessary?

No. A notebook or spreadsheet works perfectly.

7. How long does it take to see results?

Most people notice improvement within 2–3 months.

Conclusion

For many Indians, the feeling that salary is never enough is a very real struggle.

But the truth is that financial control does not always require a huge income. What matters more is awareness, structure, and consistency.

A simple budgeting system can:

- Reduce financial stress

- Help build emergency savings

- Improve spending discipline

- Create long-term financial security

Start small.

Track your expenses for one month. Build a simple budget. Save even ₹500 if that is all you can manage.

Over time, these small steps create powerful financial change.

Money management is not about perfection — it is about progress every month.

References

Reserve Bank of India Household Financial Data

https://www.rbi.org.in/

Securities and Exchange Board of India Investor Education

https://www.sebi.gov.in/

Economic Times Personal Finance Section

https://economictimes.indiatimes.com/wealth

Investopedia Budgeting Basics

https://www.investopedia.com/budgeting-4689745

Disclaimer: This article is based on personal experience and is for educational purposes only. It does not constitute financial, investment, or legal advice. Readers are advised to do their own research or consult a qualified professional before making any financial decisions.