Introduction

For most salaried Indians, income is predictable. Salary arrives on the same date every month. But expenses rarely behave the same way.

Some months are smooth. In other months, unexpected costs suddenly appear — school fees, medical bills, festivals, family functions, vehicle repairs, or even simple things like rising grocery prices.

This mismatch between fixed income and unpredictable expenses is one of the biggest financial challenges faced by middle-class Indian families.

Many people assume the solution is simply earning more. But in reality, better money management often matters more than higher income.

When income stays the same but expenses keep changing, the key is building a flexible system that can absorb shocks without destroying your savings.

In this article, we will explore:

- Why expenses fluctuate in Indian households

- Practical strategies to manage money with fixed income

- A step-by-step method to create a flexible budget

- Real-life examples from Indian families

- Common financial mistakes to avoid

If you’ve ever wondered why your monthly salary suddenly feels insufficient, this guide will help you create a practical plan.

Personal Experience

“For years I thought my salary was the problem. But when I started writing down every expense, I realised the real issue was unpredictable spending. Once I created a simple budget buffer, my finances became far less stressful.”

Understanding the Challenge: Fixed Income vs Variable Expenses

A salaried employee in India usually receives a stable monthly income. But expenses often fall into two categories:

1. Fixed Expenses

These are predictable every month.

Examples:

- Rent or home loan EMI

- School fees

- Electricity and internet

- Mobile recharge

- Insurance premiums

These expenses are easier to plan.

2. Variable Expenses

These change frequently and often surprise families.

Examples:

- Medical emergencies

- Festivals and celebrations

- Travel expenses

- Vehicle maintenance

- Unexpected social obligations

These unpredictable expenses are where most budgets collapse.

To manage this situation effectively, you must separate and control these two categories.

Why Many Indian Families Struggle With Variable Expenses

Several cultural and lifestyle factors make financial planning difficult.

1. Festival Spending

India has many festivals:

- Diwali

- Pongal

- Navratri

- Weddings and family functions

These events often involve unplanned spending.

2. Social Obligations

Indian culture values community relationships.

Expenses may include:

- Gifts

- Donations

- Family celebrations

These costs are rarely included in monthly budgets.

3. Inflation and Price Fluctuations

Prices of groceries, fuel, and utilities regularly change.

According to RBI data, inflation can significantly affect household spending patterns.

4. Lack of Financial Planning

Many households operate without structured budgeting.

You can build a stronger system by following proper personal finance planning.

Learn more in our guide on personal finance planning at https://savewithrupee.com/the-only-money-system-an-indian-family-needs-simple-sustainable-stress-free/

Key Benefits of Managing Variable Expenses Properly

Creating a flexible money system offers several advantages.

Better Financial Stability

Unexpected expenses will not destroy your monthly budget.

Reduced Financial Stress

Knowing that you have a buffer reduces anxiety.

Consistent Savings

Even when expenses fluctuate, savings remain protected.

Long-Term Financial Growth

Once spending is controlled, you can start investing slowly.

Step-by-Step Guide to Managing Money With Fixed Income

Here is a practical system that works well for most Indian households.

Step 1: Track All Expenses for One Month

Before changing anything, observe your current spending.

Record:

- Groceries

- Transport

- Online purchases

- Food delivery

- Medical expenses

This reveals spending patterns.

Many families are surprised to discover hidden expenses they never noticed.

If you want to understand spending leaks better, read this article:

Learn more in our guide on saving money tips at https://savewithrupee.com/where-most-indian-households-lose-money-without-realising-hidden-leaks-explained/

Step 2: Divide Expenses Into Three Categories

A simple system works best.

Category 1: Fixed Expenses

Example:

- Rent

- EMI

- School fees

Category 2: Variable Essential Expenses

Example:

- Groceries

- Fuel

- Utilities

Category 3: Lifestyle Expenses

Example:

- Eating out

- Shopping

- Entertainment

This separation helps you identify where adjustments are possible.

Step 3: Create a “Monthly Buffer Fund”

A buffer fund protects your budget from variable expenses.

Example:

Monthly salary: ₹40,000

| Category | Amount |

|---|---|

| Fixed expenses | ₹20,000 |

| Variable expenses | ₹12,000 |

| Buffer fund | ₹4,000 |

| Savings | ₹4,000 |

This ₹4,000 buffer handles surprises without touching savings.

Step 4: Plan for Annual Expenses

Many expenses occur only once or twice per year.

Examples:

- Insurance premiums

- School admissions

- Festivals

- Vehicle servicing

Divide these costs across 12 months.

Example:

Annual festival spending = ₹12,000

Monthly allocation = ₹1000

This prevents sudden financial pressure.

Step 5: Use Weekly Spending Limits

Instead of managing money monthly, divide it weekly.

Example:

Variable expenses = ₹12,000

Weekly limit = ₹3000

This prevents overspending early in the month.

You can also explore detailed budgeting systems here:

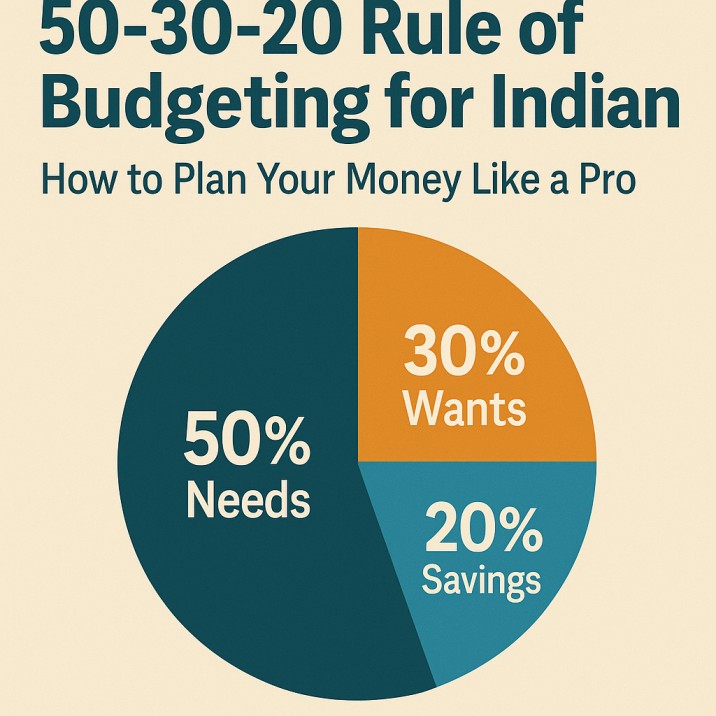

Learn more in our guide on monthly budgeting guide at https://savewithrupee.com/50-30-20-rule-of-budgeting-for-indians-in-2025-how-to-plan-your-money-like-a-pro/

Step 6: Automate Savings First

Savings should not depend on leftover money.

Instead, save immediately when salary arrives.

Examples:

- SIP investment

- Recurring deposit

- Emergency fund contribution

If you’re starting with investments, read:

Learn more in our guide on best investment options in India at https://savewithrupee.com/sip-for-beginners-start-with-₹500/

Comparison of Money Management Methods

| Feature | Traditional Budget | Flexible Budget | Envelope Method |

|---|---|---|---|

| Handles variable expenses | Poor | Good | Excellent |

| Easy for beginners | Medium | Easy | Very easy |

| Requires apps | Sometimes | Optional | No |

| Best for Indian families | Medium | High | High |

Most families benefit from flexible budgeting combined with envelope spending.

Real-Life Example: A ₹35,000 Salary Household

Consider the example of Priya, a school teacher in Chennai.

Before Budget Planning

Her monthly spending looked like this:

| Expense | Amount |

|---|---|

| Rent | ₹9000 |

| Groceries | ₹7000 |

| Transport | ₹3000 |

| Random spending | ₹9000 |

| Savings | ₹0–₹1000 |

Every few months, unexpected expenses forced her to borrow money.

After Budget System

She created a buffer system.

| Category | Amount |

|---|---|

| Fixed expenses | ₹19,000 |

| Variable expenses | ₹10,000 |

| Buffer | ₹3000 |

| Savings | ₹3000 |

Within a year, she built ₹36,000 emergency savings.

Small planning created huge financial relief.

Common Mistakes When Managing Variable Expenses

Avoid these errors.

Ignoring Small Expenses

Food delivery, subscriptions, and online shopping quietly increase spending.

Not Planning for Festivals

Festival costs often damage budgets.

Using Credit Cards for Emergencies

Credit cards should not replace emergency funds.

Saving Only What Is Left

Savings should be planned first.

Not Tracking Money

Untracked spending leads to financial confusion.

Expert Tips for Better Money Control

Build an Emergency Fund

Every Indian family should keep at least 3–6 months of expenses saved.

Learn more in our guide on emergency fund guide at

https://savewithrupee.com/emergency-fund-for-indian-families-how-much-you-really-need-where-to-keep-it-savewithrupee/

Reduce Lifestyle Inflation

When income increases, expenses often rise too.

Maintain the same lifestyle while increasing savings.

Create Small Side Income

Even an additional ₹3000–₹5000 monthly can significantly improve financial stability.

Explore ideas here:

Learn more in our guide on passive income ideas at https://savewithrupee.com/passive-income-ideas-in-india-2025-12-real-ways-to-earn-while-you-sleep/

Track Spending Weekly

Weekly review keeps your budget on track.

Pros and Cons of Flexible Budgeting

| Pros | Cons |

|---|---|

| Handles unpredictable expenses | Requires regular monitoring |

| Reduces financial stress | Needs discipline |

| Protects savings | Takes time to master |

| Improves financial awareness | Initial setup required |

Frequently Asked Questions

1. What is the biggest challenge with fixed income?

Unpredictable expenses such as medical costs, repairs, or festival spending.

2. How much buffer should I keep monthly?

Ideally 10% of your income.

3. Is budgeting necessary if my salary is small?

Yes. Budgeting is even more important for smaller incomes.

4. Should I save or pay expenses first?

Always save first.

5. How much should Indians ideally save monthly?

Experts recommend 20% savings, but even 5–10% is a good start.

6. What if unexpected expenses exceed my buffer?

Use your emergency fund, not credit cards.

7. How long does it take to see financial improvement?

Most people see improvement within 3–4 months of consistent budgeting.

Conclusion

Managing money when income is fixed but expenses are unpredictable is a reality for most Indian households.

The goal is not to eliminate variable expenses — that is impossible.

Instead, the solution is building a flexible financial system that includes:

- Clear expense tracking

- A monthly buffer fund

- Planned savings

- Emergency reserves

Once these systems are in place, unexpected expenses become manageable rather than stressful.

Financial stability does not come from earning the highest salary. It comes from managing the money you already have wisely.

Start small. Track your expenses. Create a buffer. Save consistently.

Over time, these habits will transform your financial life.

References

Reserve Bank of India Household Finance Reports

https://www.rbi.org.in

Securities and Exchange Board of India – Investor Education

https://www.sebi.gov.in

Economic Times – Personal Finance Section

https://economictimes.indiatimes.com/wealth

Investopedia – Budgeting Basics

https://www.investopedia.com/budgeting-4689745

Personal Experience

“Over the years, I’ve noticed that most financial problems don’t come from low income, but from lack of planning and awareness. Even small changes in spending habits can make a big difference.”

“In my own journey, tracking expenses and following a simple budget helped me reduce stress and gain better control over money. These are practical lessons any Indian household can apply.”

References

- Reserve Bank of India – Financial Reports

- SEBI Investor Education

- Economic Times – Personal Finance

- Investopedia – Budgeting & Finance Basics

Disclaimer: This article is based on personal experience and is for educational purposes only. It does not constitute financial, investment, or legal advice. Readers are advised to do their own research or consult a qualified professional before making any financial decisions.