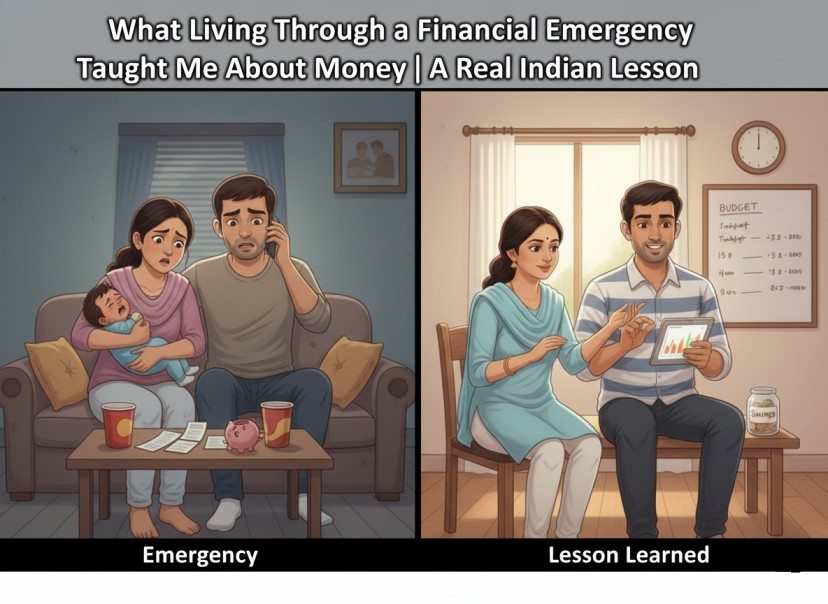

A real financial emergency changed how I see money forever. Honest lessons about savings, habits, insurance, and peace—by Save With Rupee’s founder.

🚑 What Living Through a Financial Emergency Taught Me About Money

(A real Indian experience that changed everything)

There are moments in life that quietly divide your story into before and after.

For me, it wasn’t a promotion.

It wasn’t buying my house.

It wasn’t even getting my car.

It was a financial emergency.

One that didn’t announce itself loudly.

One that didn’t come with drama.

But one that exposed every weakness in my money life.

If you’ve never faced a financial emergency, this article might save you years of stress.

If you already have, this article might feel painfully familiar.

🙋♂️ Who I Am (Why This Story Is Real)

My name is H. Suresh,

a finance content creator from Chennai, Tamil Nadu, and founder of SaveWithRupee.com.

For over 10 years, I’ve researched and written about:

- Saving money in India

- Budgeting for real families

- Income ideas that actually work

- Financial habits that create peace, not pressure

Smarter Money. Better Life. One Rupee at a Time.

This story is not theory.

It’s lived experience.

⏳ Life Before the Emergency (The Illusion of “I’m Managing”)

At that time:

- Salary was coming regularly

- Bills were paid

- Life looked “normal”

But behind the scenes:

- ❌ No proper emergency fund

- ❌ Savings mixed with spending

- ❌ Insurance not fully planned

- ❌ Confidence without preparation

I told myself:

“Kuch ho bhi gaya toh manage ho jayega.”

That sentence almost always comes before trouble.

⚠️ The Emergency (When Money Stops Being Numbers)

I won’t go into personal details out of respect,

but it involved:

- Sudden, unavoidable expense

- Tight deadline

- No time to “plan”

What shocked me was not the amount.

What shocked me was the panic.

😰 What I Felt in Those Moments

- Fear (pure, silent fear)

- Guilt (“I should have prepared”)

- Helplessness

- Shame (especially as someone who writes about money)

I realised something deeply uncomfortable:

Knowing about money is useless

if your system isn’t ready.

💳 The Ugly Reality I Faced

Here’s what actually happened:

- Savings were less than I imagined

- Money was scattered

- Decisions had to be rushed

- Emotional pressure affected judgment

Every rupee felt heavier than usual.

🧠 Lesson #1: Emergency Fund Is Not Optional

This was the biggest lesson.

An emergency fund is not:

- A luxury

- A “later” goal

- A rich-people thing

It is basic survival.

If I had followed this earlier:

👉 Emergency Fund – How Much Should an Indian Household Keep?

…the situation would have felt manageable, not terrifying.

😔 Lesson #2: Stress Makes Money Decisions Worse

When you’re calm:

- You think logically

- You compare options

- You negotiate

When you’re stressed:

- You rush

- You accept bad terms

- You regret later

I learned that:

Financial emergencies don’t just cost money.

They cost mental clarity.

🧾 Lesson #3: Liquidity Matters More Than Returns

Before this incident, I obsessed over:

- Interest rates

- Returns

- “Best” options

During the emergency, only one thing mattered:

How fast can I access cash?

That’s when I understood the role of:

- Savings accounts

- Liquid funds

- Proper separation of money

👉 Related understanding:

Government Schemes Indians Ignore That Quietly Beat Bank Savings

💸 Lesson #4: Credit Is a Tool, Not a Backup Plan

I saw people around me say:

“Credit card hai na.”

But in emergencies:

- Credit comes with pressure

- Interest adds insult to injury

- Long-term stress increases

I promised myself:

I will never use debt as my first line of defence again.

👉 If you’re already stuck, read this:

Credit Card Debt in India – Smart Payoff Plan

🛡️ Lesson #5: Insurance Is Emotional Protection

Before the emergency, insurance felt:

- Boring

- Unnecessary

- “Waste if unused”

After the emergency:

- It felt like peace

- Like backup

- Like quiet confidence

I finally understood:

Insurance doesn’t save money.

It saves your life from financial collapse.

👉 Practical guide:

Insurance Premium Saving Tips India

🧍♂️ Lesson #6: Financial Emergencies Test Your Habits, Not Income

This emergency would have hurt:

- At low income

- At higher income

Why?

Because habits decide preparedness.

This connects deeply with:

The Day I Realised My Salary Wasn’t the Problem—My Habits Were

🔄 Lesson #7: Shame Delays Recovery

One thing I noticed in myself:

- I didn’t want to talk about it

- I felt embarrassed

- I wanted to “handle it alone”

That silence makes emergencies worse.

Money conversations matter.

👉 Helpful perspective:

Why Family Budget Plan Is Important

📉 What Went Wrong (My Honest Mistakes)

- ❌ Emergency fund not prioritised

- ❌ Overconfidence

- ❌ Mixing savings with expenses

- ❌ Delaying insurance

- ❌ Assuming “nothing will happen”

👉 More honesty here:

My Biggest Regret About Money

🧠 Myth vs Reality (Learned the Hard Way)

| Myth ❌ | Reality ✅ |

|---|---|

| Emergency won’t happen to me | It happens to everyone |

| I’ll manage somehow | Planning is easier than panic |

| Savings can wait | Emergencies don’t wait |

| Insurance is optional | It’s essential |

🪜 What I Changed After the Emergency (Step-by-Step)

✅ Step 1: Separate Emergency Money

No mixing. No touching.

✅ Step 2: Build Slowly but Consistently

₹5,000 → ₹10,000 → ₹25,000 → more.

✅ Step 3: Automated Savings

No reliance on willpower.

👉 Helpful guide:

How to Save ₹5,000 Every Month Without Sacrifice

✅ Step 4: Insurance Review

Health + term.

✅ Step 5: Family Awareness

No secrets. No confusion.

📊 Before vs After (My Personal Shift)

| Area | Before Emergency | After Emergency |

|---|---|---|

| Emergency fund | Weak | Priority |

| Stress | High | Controlled |

| Money clarity | Low | High |

| Insurance | Delayed | Active |

| Confidence | False | Real |

🧾 Emergency-Readiness Checklist

✔ Emergency fund started

✔ Liquidity available

✔ Insurance active

✔ Credit under control

✔ Family informed

Tick 3+, and you’re safer than you think.

👍 Pros & Cons of Learning This Lesson the Hard Way

Pros

- Permanent mindset shift

- Better discipline

- Calm decision-making

- Long-term peace

Cons

- Emotional cost

- Stressful experience

- Wish I learned earlier

🏆 Editor’s Pick (The One Line That Stays With Me)

“Money shows its true value

when things go wrong.”

This lesson shaped everything I write on SaveWithRupee.com today.

❓ FAQs (From Readers Who’ve Been There)

1. How big should an emergency fund be?

At least 6 months of expenses.

2. What if income is small?

Start small. Protection matters more than amount.

3. Should I stop investing to build emergency fund?

Temporarily, yes.

4. Can insurance replace emergency fund?

No. They work together.

5. Are emergencies predictable?

No. That’s the point.

6. Should families discuss emergencies?

Absolutely.

7. What’s the first step today?

Separate ₹1,000. Start.

❤️ Final Words (From Someone Who’s Been There)

I don’t wish a financial emergency on anyone.

But if it happens, I want you to remember this:

Preparation turns panic into inconvenience.

Lack of preparation turns inconvenience into trauma.

That emergency made me a better money manager,

a calmer person,

and a more honest guide.

That’s why SaveWithRupee.com exists —

so you don’t have to learn everything the hard way.

🚀 Strong Call To Action (CTA)

If this story made you pause, don’t delay.

👉 Start here today:

7 Steps to Become Financially Independent

Bookmark SaveWithRupee.com

— where Indian money advice is real, tested, and human.

Smarter Money. Better Life. One Rupee at a Time. 💚

Author Insight

In my own experience managing monthly expenses in India, I realized that the biggest financial problems were not due to low income, but due to lack of planning. For example, when my monthly income was around ₹25,000, I often ended up spending almost everything without saving anything at the end of the month.”

“I started tracking my expenses daily using a simple notebook. Within one month, I noticed that small, unnecessary expenses like frequent online orders and unplanned spending were taking a large portion of my income.”

“By making small changes—like setting a fixed budget for groceries, limiting online purchases, and saving at least ₹2,000 at the beginning of each month—I was able to reduce financial stress and slowly build better control over my money.” “These are simple and practical methods that any Indian household can follow without needing complex financial knowledge.”

Research Sources

- Reserve Bank of India – Financial Reports

- SEBI Investor Education

- Economic Times – Personal Finance

- Investopedia – Budgeting & Finance Basics

Disclaimer: This article is based on personal experience and is for educational purposes only. It does not constitute financial, investment, or legal advice. Readers are advised to do their own research or consult a qualified professional before making any financial decisions.